---This article is a 14 minute read.---

By the 1970’s over 40% of employees had a pension, a guarantee from their employer that they would get a good percentage of their salary and benefits upon retirement. Employees did not have to manage their retirement or even know how to invest, their pension ensured secured income for the rest of their life.

Unfortunately, pensions became a huge danger to employers for several reasons, here are just a few:

Unfortunately, pensions became a huge danger to employers for several reasons, here are just a few:

- People started to live longer, costing employers to pay out much more than expected.

- Market volatility became greater than projected causing employers to be inadequately prepared. For example, during initial forecasts, employers anticipated earning a certain amount on the money they put away per employee and as that amount that was put away grew, they would have plenty of money to pay the guaranteed retirement. Regrettably, the actual return on investment was far less than the initial projected return leaving the employer accounts severely underfunded.

- Global competition and employment. Companies like IBM, Verizon Communications, Delta Airlines, The Boeing Company, General Motors, American Airlines and thousands more were forced to compete with new rivals who didn’t bear the cost of old-style benefits and that is why each of the aforementioned companies eventually “restructured” or eliminated their pension plans.

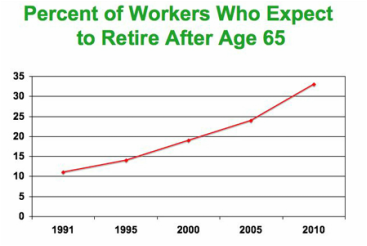

This graph summarizes information from the Employee Benefit Research Institute's 2010 Retirement Confidence Survey (RCS)

This graph summarizes information from the Employee Benefit Research Institute's 2010 Retirement Confidence Survey (RCS) In 1978, the 401(k) plan was invented. The 401(k) started as an investment vehicle primarily for high income earners that had extra capital that they could put away tax deferred. For example, if an employee earned $100,000, he could invest $10,000 into the 401(k) and would only be taxed that year as if he/she only made $90K. In addition to the tax benefit, and unlike a defined pension, the 401(k) was portable, you could take it with you from one employer to the next. By 1981, more than half of all large firms offered a 401(k) plan.

The 401(k) plan was intended to be a savings plan that was offered in addition to a pension plan.

A game changer occurred in 1986 when Congress replaced the defined benefit plan for federal civilian workers with a far less generous defined benefit plan and a 401(k)-type plan. This was seen as an endorsement of the 401(k) and since that time, 401(k) plans have become the fastest-growing type of retirement plan in the United States.

Due to the risks associated with defined benefits virtually all employers that offered pensions have significantly modified them to be far less favorable, no longer provide defined benefits to new employees hired after a cutoff date, or have gotten rid of them all together. Today, 94% of private employers offer a 401(k). 401(k)s, which were never designed to be the primary method of saving for retirement, have now become just that.

The old way of doing business, guaranteeing employees an income for life, became too challenging, costly, and unpredictable. Now the game has changed. It is entirely up to the employee to invest for his/her retirement. So, how have 401(k)’s performed since they began nearly 40 years ago? The short answer…not too good.

According to Fidelity, one of the largest 401(k) providers in the world, the average 401K balance is now around $91,800 as of 7/1/2015. Vanguard, another large 401(k) provider, boasts and average 401(k) balance of $101,650. According to Fidelity, about half of a percent (0.5%) of Fidelity 401(k) participants have hit the $1 million mark. On average the 401(k) millionaires contributed 14% of their pay (not including company matching), worked at their company for more than 30 years, and made less than $150,000 per year.

The statistics are shocking. According to the U.S. Census Bureau and Bankrate, more than 99% of people age 65 today have less than $1 million in retirement savings. One million dollars isn’t what it use to be and still most Americans will never achieve it in their 401(k).

The Government Accountability Office (GAO) recently released a report on mega-IRA’s, IRAs in excess of $5 million. The GAO figures if someone had maxed out every year from 1975-2011, invested in an S&P index fund (which returned an average of about 8 percent annually), and never withdrew a dime, they’d have about $353,000.

The 401(k) plan was intended to be a savings plan that was offered in addition to a pension plan.

A game changer occurred in 1986 when Congress replaced the defined benefit plan for federal civilian workers with a far less generous defined benefit plan and a 401(k)-type plan. This was seen as an endorsement of the 401(k) and since that time, 401(k) plans have become the fastest-growing type of retirement plan in the United States.

Due to the risks associated with defined benefits virtually all employers that offered pensions have significantly modified them to be far less favorable, no longer provide defined benefits to new employees hired after a cutoff date, or have gotten rid of them all together. Today, 94% of private employers offer a 401(k). 401(k)s, which were never designed to be the primary method of saving for retirement, have now become just that.

The old way of doing business, guaranteeing employees an income for life, became too challenging, costly, and unpredictable. Now the game has changed. It is entirely up to the employee to invest for his/her retirement. So, how have 401(k)’s performed since they began nearly 40 years ago? The short answer…not too good.

According to Fidelity, one of the largest 401(k) providers in the world, the average 401K balance is now around $91,800 as of 7/1/2015. Vanguard, another large 401(k) provider, boasts and average 401(k) balance of $101,650. According to Fidelity, about half of a percent (0.5%) of Fidelity 401(k) participants have hit the $1 million mark. On average the 401(k) millionaires contributed 14% of their pay (not including company matching), worked at their company for more than 30 years, and made less than $150,000 per year.

The statistics are shocking. According to the U.S. Census Bureau and Bankrate, more than 99% of people age 65 today have less than $1 million in retirement savings. One million dollars isn’t what it use to be and still most Americans will never achieve it in their 401(k).

The Government Accountability Office (GAO) recently released a report on mega-IRA’s, IRAs in excess of $5 million. The GAO figures if someone had maxed out every year from 1975-2011, invested in an S&P index fund (which returned an average of about 8 percent annually), and never withdrew a dime, they’d have about $353,000.

I believe I know why so many retirement accounts have such small value relative to what it takes to retire. True, according to Bankrate, more than 50% of Americans don’t invest at all (no stocks, no IRA, no 401(k)). Yikes! That’s not the reason. I believe the main reason why those that diligently save in their 401(k)s rarely have success is due to the investment choices available within most 401(k)s.

Most 401(k)s are riddled with mutual funds. A mutual fund is simply a basket of stocks with an added management fee. The initial concept was to have a fund professionally managed by experts that chose only the “winners” and because it’s a basket of stocks, you could buy one fund and now you were “diversified”. For example, let’s say that the ABC Technology Fund consists of 20% Apple stock, 20% Google stock, 20% IBM stock, 20% Amazon stock, 20% Microsoft stock, and let’s not forget the ABC Technlogy Fund “management fee”. By circumventing the ABC Technology Fund and buying the exact same stocks outright, you would eliminate the management fee thereby guaranteeing you to always outperform the ABC Technology Fund. This is why no billionaire on earth uses mutual funds as a wealth building strategy and also why the owners of Fidelity, one of the largest mutual fund companies in America, own no mutual funds themselves. Unfortunately, mutual funds are here to stay because whether you win or lose, the mutual fund manager makes a profit because of the built-in fee; a fee that most people don’t even realize exists. Again, the point of a mutual fund is to outperform the general stock market by only picking the winners, so why is it acceptable that 94% of the time mutual funds UNDERperform the stock market (e.g. mutual funds virtually always underperform major indices like the S&P 500 or the Dow Jones)? How do you get ahead when you’re ALWAYS underperforming? To be clear, I believe the single greatest threat to the success of the 401(k) saver is the investments he/she has to pick from inside of his/her 401(k) plan.

So how do we fix this? Should we all avoid 401(k)s? What can we do?

A great alternative to a 401(k) is to start a self-directed 401(k) and/or IRA. You can rollover your money from your current 401(k), without penalties or tax consequences, into a self-directed plan and from that self-directed plan you can invest in virtually anything including physical gold and real estate. Let me be clear, you’re not withdrawing the money, you’re rolling it over. If you’re one of those that believes the 401(k) plan is good enough as is, imagine rolling over your money to a self-directed plan and mirroring your previous 401(k) by purchasing all the same stocks outright and eliminating the mutual fund fee…an instant gain. Even the most skeptical or so-called conservative investor could benefit greatly from using a self-directed plan. If your current 401(k) will not let you rollover while still employed with them, contact me and I’ll show you other legal and acceptable ways around it.

Most 401(k)s are riddled with mutual funds. A mutual fund is simply a basket of stocks with an added management fee. The initial concept was to have a fund professionally managed by experts that chose only the “winners” and because it’s a basket of stocks, you could buy one fund and now you were “diversified”. For example, let’s say that the ABC Technology Fund consists of 20% Apple stock, 20% Google stock, 20% IBM stock, 20% Amazon stock, 20% Microsoft stock, and let’s not forget the ABC Technlogy Fund “management fee”. By circumventing the ABC Technology Fund and buying the exact same stocks outright, you would eliminate the management fee thereby guaranteeing you to always outperform the ABC Technology Fund. This is why no billionaire on earth uses mutual funds as a wealth building strategy and also why the owners of Fidelity, one of the largest mutual fund companies in America, own no mutual funds themselves. Unfortunately, mutual funds are here to stay because whether you win or lose, the mutual fund manager makes a profit because of the built-in fee; a fee that most people don’t even realize exists. Again, the point of a mutual fund is to outperform the general stock market by only picking the winners, so why is it acceptable that 94% of the time mutual funds UNDERperform the stock market (e.g. mutual funds virtually always underperform major indices like the S&P 500 or the Dow Jones)? How do you get ahead when you’re ALWAYS underperforming? To be clear, I believe the single greatest threat to the success of the 401(k) saver is the investments he/she has to pick from inside of his/her 401(k) plan.

So how do we fix this? Should we all avoid 401(k)s? What can we do?

A great alternative to a 401(k) is to start a self-directed 401(k) and/or IRA. You can rollover your money from your current 401(k), without penalties or tax consequences, into a self-directed plan and from that self-directed plan you can invest in virtually anything including physical gold and real estate. Let me be clear, you’re not withdrawing the money, you’re rolling it over. If you’re one of those that believes the 401(k) plan is good enough as is, imagine rolling over your money to a self-directed plan and mirroring your previous 401(k) by purchasing all the same stocks outright and eliminating the mutual fund fee…an instant gain. Even the most skeptical or so-called conservative investor could benefit greatly from using a self-directed plan. If your current 401(k) will not let you rollover while still employed with them, contact me and I’ll show you other legal and acceptable ways around it.

If you’ve never heard of a self-directed 401(k) and/or IRA, don’t be embarrassed. Although they’ve been around for over 30 years, 96% of Americans don’t have or haven’t heard of them! This is not by accident, wall street and main street investment firms want you to use mutual funds and billions if not trillions of dollars have been spent over several decades teaching you that mutual funds were safe and good for your retirement account. There are several self-directed custodians out there and although I can’t endorse any particular one, I would suggest you take a look at Equity Trust Company, they currently have over 130,000 clients in all 50 states and manage about $12 billion in retirement plan assets. I was recently invited to speak at an Equity Trust Wealth Building Event where I shared simple, common sense, strategies on how to create wealth investing in real estate inside of a self-directed retirement account.

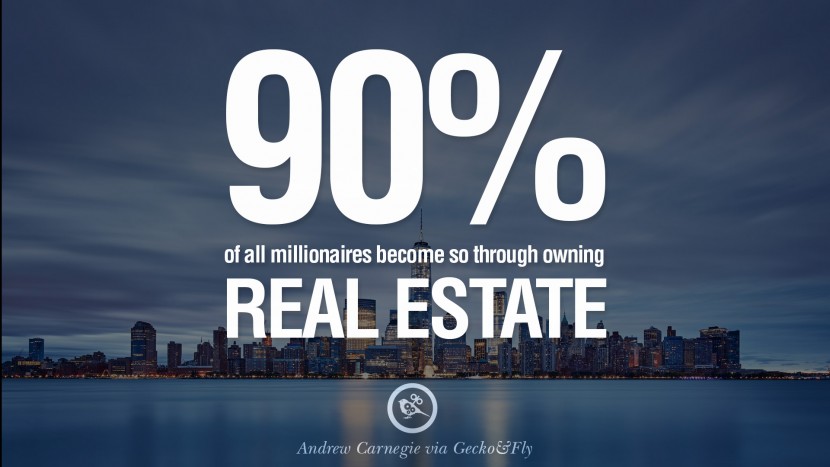

I’m sure you’re aware that more millionaires have been created in real estate than in any other industry. So why not invest in real estate? Why gamble on mutual funds? Warren Buffett does not invest in mutual funds. John C. Bogle, founder and former CEO of the Vanguard Group, one of the world’s largest mutual fund companies, does not invest in mutual funds. Bogle says, “96% of all mutual funds don’t match the market over any ten year period.” Ouch. The founder of one of the largest mutual fund companies in the world openly speaks against mutual funds yet most middle-class Americans still believe mutual funds are how you “play it safe”.

I’m sure you’re aware that more millionaires have been created in real estate than in any other industry. So why not invest in real estate? Why gamble on mutual funds? Warren Buffett does not invest in mutual funds. John C. Bogle, founder and former CEO of the Vanguard Group, one of the world’s largest mutual fund companies, does not invest in mutual funds. Bogle says, “96% of all mutual funds don’t match the market over any ten year period.” Ouch. The founder of one of the largest mutual fund companies in the world openly speaks against mutual funds yet most middle-class Americans still believe mutual funds are how you “play it safe”.

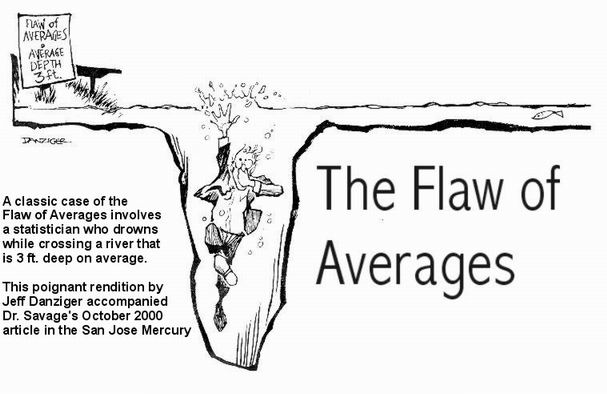

Sam Savage's book The Flaw of Averages: Why We Underestimate Risk in the Face of Uncertainty. This cartoon says it all.

How about those top performing mutual funds we’ve all seen that seem to have outperformed the market? Bogle says, “Surprise, the returns reported by mutual funds aren’t actually earned by investors. A firm will go out and start five incubation funds, and they will try and shoot the lights out with all five of them. And of course they don’t with four of them, but they do with one. So they drop the other four and take the one that did very well public with a great track record and sell that track record. An ‘insider’ knows that chasing the high flyer advertised fund is chasing the wind.”

I ask again, why not learn how to invest in real estate? 77% of millionaires invest in real estate. Yes, I already mentioned that more millionaires have been made in real estate than in any other industry. That is why I suggest investing in real estate or other real assets like gold and silver. You can do this all in your self-directed 401(k) and/or IRA. Several millionaires and billionaires use self-directed 401(k)s and IRAs.

Facebook cofounder Dustin Moskovitz has earned over $95 million in his self-directed Roth IRA [a Roth is tax-free retirement account].

Mitt Romney recently ran for president and he had amassed $100 million in his self-directed IRA. Let me let you in on a secret, he didn’t amass that type of wealth using mutual funds.

The point is, if you want to amass real wealth in your retirement account you have to take a look at using an account that will allow you to invest in assets that have a track record for creating millionaires like real estate. The starting point is to get educated. Understand what a self-directed 401(k) and/or IRA is and the very many ways to use it to your advantage. Also, learn from others that have had success in their self-directed accounts.

If you’d like to learn about proven real estate strategies and how to start on the fast track to wealth be sure to attend our next event.

Facebook cofounder Dustin Moskovitz has earned over $95 million in his self-directed Roth IRA [a Roth is tax-free retirement account].

Mitt Romney recently ran for president and he had amassed $100 million in his self-directed IRA. Let me let you in on a secret, he didn’t amass that type of wealth using mutual funds.

The point is, if you want to amass real wealth in your retirement account you have to take a look at using an account that will allow you to invest in assets that have a track record for creating millionaires like real estate. The starting point is to get educated. Understand what a self-directed 401(k) and/or IRA is and the very many ways to use it to your advantage. Also, learn from others that have had success in their self-directed accounts.

If you’d like to learn about proven real estate strategies and how to start on the fast track to wealth be sure to attend our next event.

RSS Feed

RSS Feed